In the UK, the price of alcoholic drinks has increased by almost 300% from 19871 to 2017, with UK prices currently considered among the highest in the EU2. Alcohol consumption has decreased in the last decade3, but with no reduction in the detrimental effects of excessive intake (HSCIC, 2016), which causes an economic burden estimated at £51 billion/year (Burton et al., 2017).

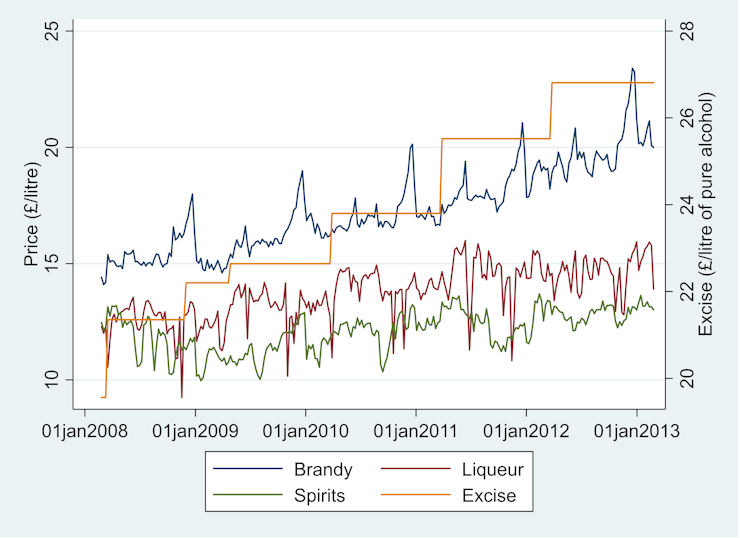

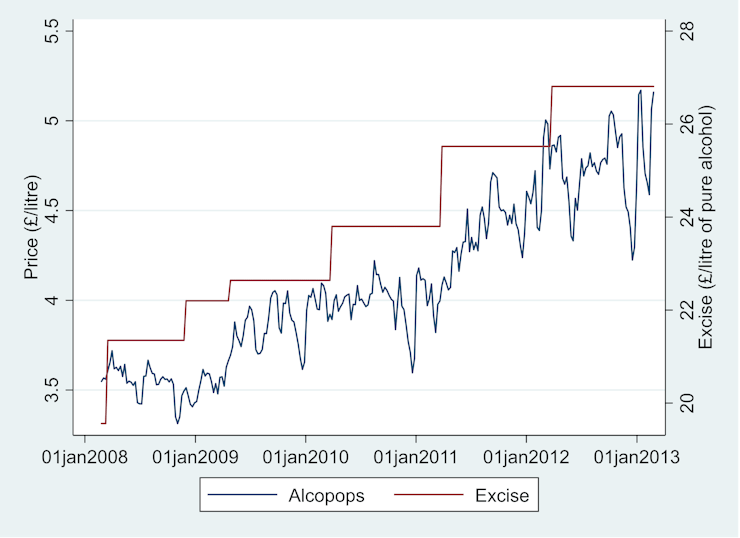

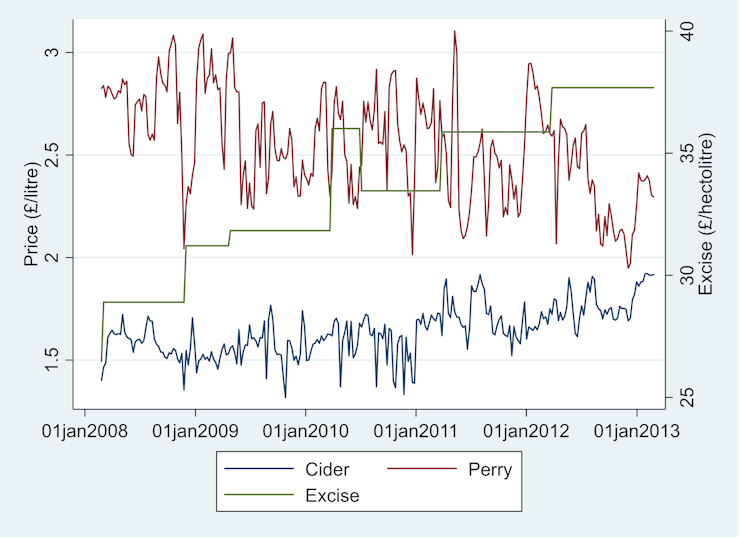

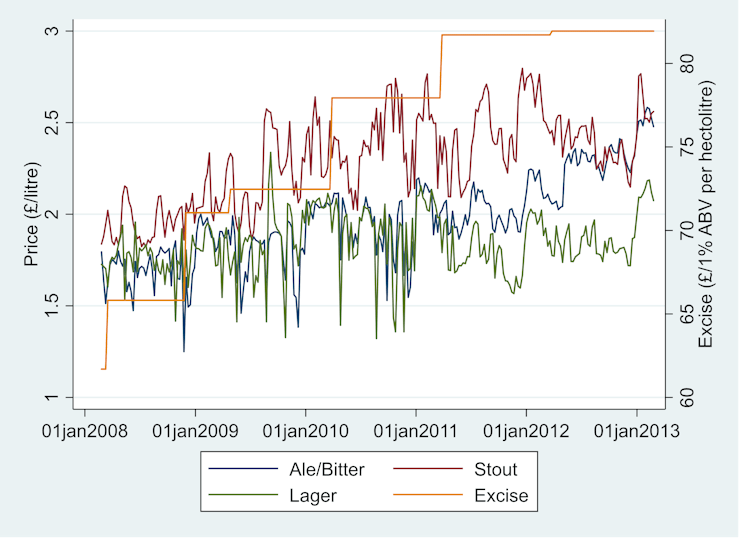

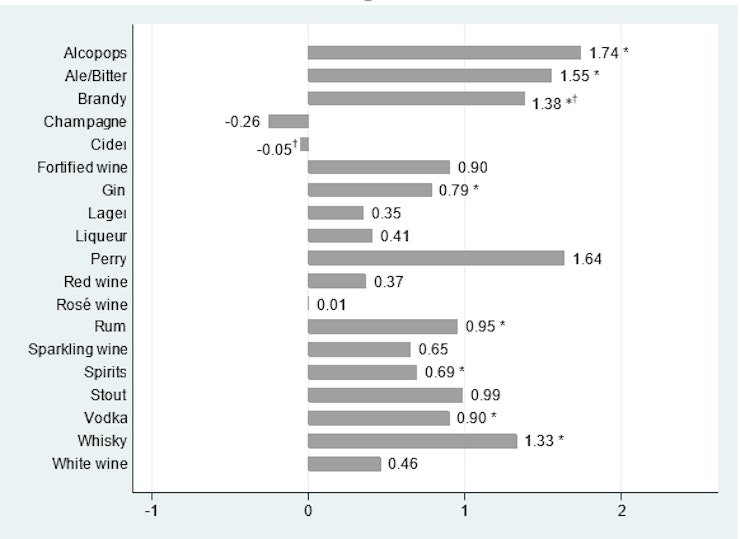

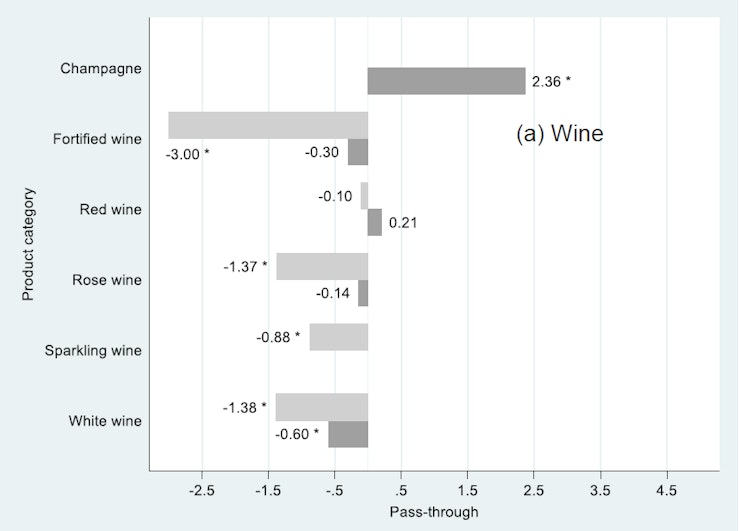

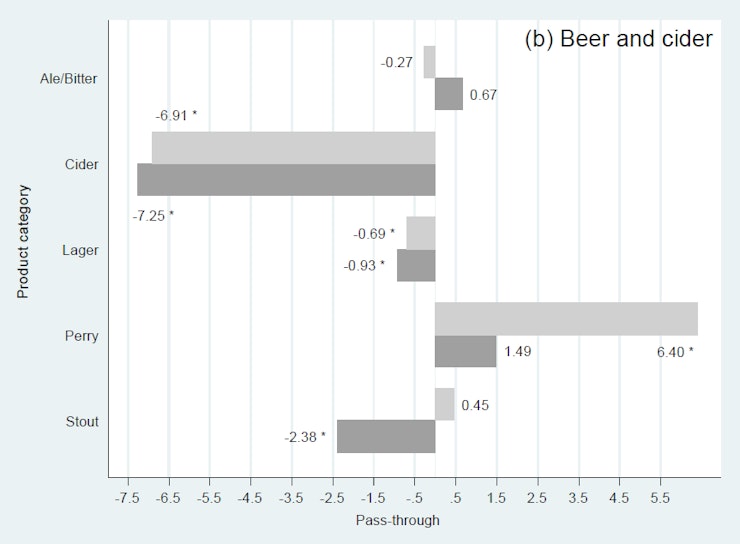

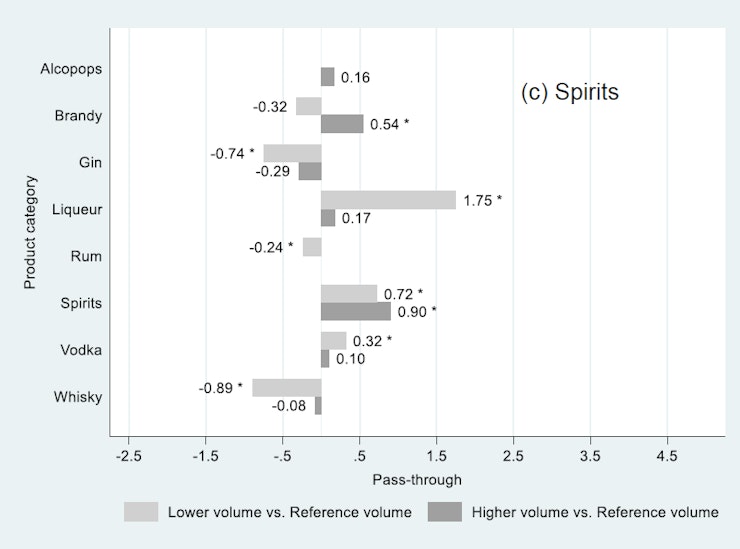

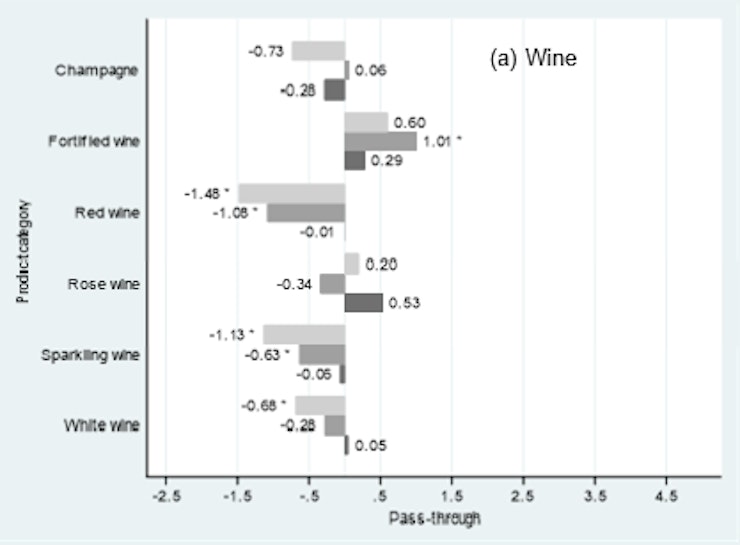

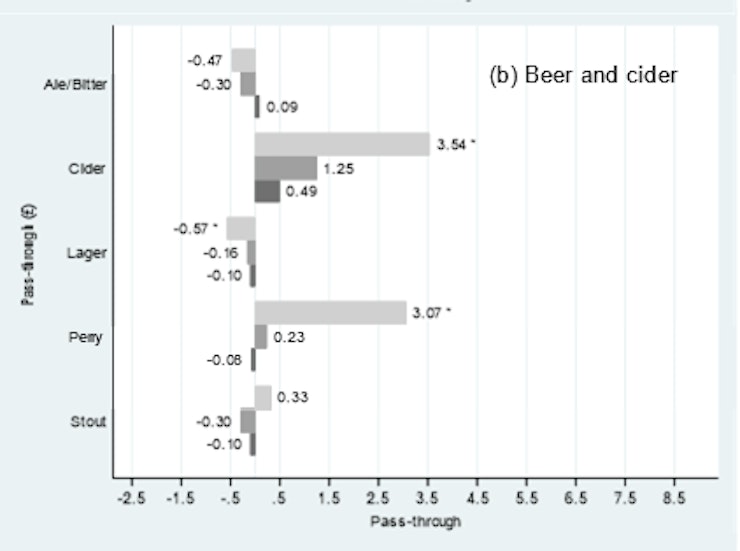

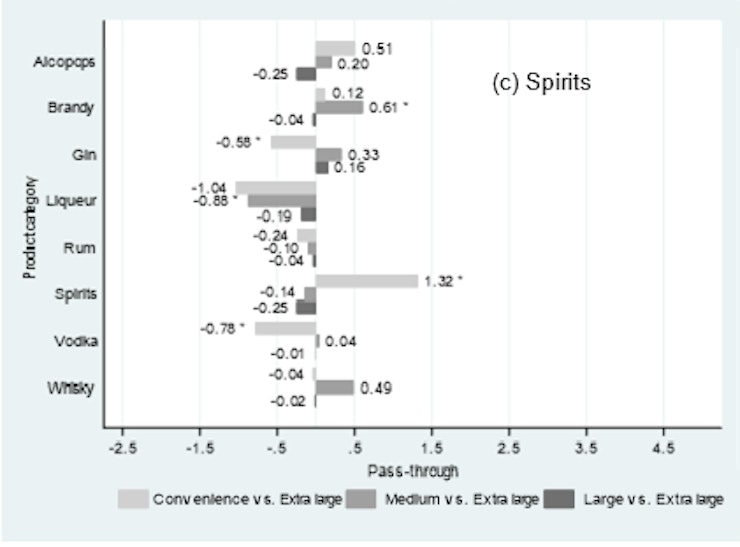

The main policy to tackle alcohol overconsumption in the UK has been through alcohol excises, which charge tax consumers proportionally to the quantity they consume – so that heavy drinkers pay more tax than occasional ones. However, taxation can drive behaviour only if the increase in costs imposed by the tax is effectively translated into higher prices at the point of purchase (e.g. Weyl and Fabinger, 2013; Bonnet et al., 2013). This concept, known as tax pass-through, reflects the extent to which the tax is passed onto the price the consumer pays or is (partially) absorbed by the retailer or manufacturer (Fullerton and Metcalf, 2002).

Notably, a £1 tax increase can increase prices by: £0 (zero pass-through) if the supplier absorbs the whole tax; a value strictly between £0 and £1 (under-shifting) if the supply side of the market offsets the increase in price by reducing costs, e.g. labour costs; £1 (full pass-through) when consumers pay the full extent of the tax; or more than £1 (over-shifting) when suppliers facing an inelastic demand increase prices by more than the value of the tax to retain profits. See also Fullerton and Metcalf (2002) for more detail.

In the UK, alcohol excises have increased supermarket prices, but less so for low-priced drinks compared to expensive ones (Ally et al., 2014). Looking only at the prices that retailers charge for alcohol, however, does not provide an indication of the impact of taxation on the prices of alcoholic drinks paid by consumers. In fact, consumers can adjust to price increases by shifting to equivalent products that fit within their original price range in what is called product substitution (DeCicca et al., 2012). For example, consumers can shift to a cheaper category (e.g. beer instead of wine); to a cheaper subcategory within the same excise category (e.g. a vodka-based alcopop instead of pure vodka); or to a cheaper product within the same category (e.g. buying red wine as usual but a cheaper brand).